Commercial Owners Seeking Temporary Property Tax Reduction for 2025-2026

The Assessor’s Office has the authority to temporarily reduce property tax assessments in accordance with Proposition 8 based if the market value—as of January 1—falls below factored base year value (Prop 13 value). Proposition 8 only allows for temporary reductions on land and buildings. However, tenants, such as hair and nail salons or restaurants, may receive reductions through a property owner in accordance with their lease.

Data will continue to be accepted up to August 1, 2025. Below are examples of the requested industry-specific data. This information will be used by the Assessor’s Office to evaluate potential opportunities to reduce 2025-2026 property taxes for commercial properties.

To apply for a reduction, applicants are encouraged to have the above data compiled electronically prior to completing the on-line application below.

Information needed by Assessor's office from all Owners:

- Best estimate of prospective income and expense statements for the 2025 calendar year.

- Actual income and expense statements for the 2023 and 2024 calendar years.

- Description and actual cost of any new construction completed or in progress, during the 2024 calendar year.

- Copy of any appraisal performed on the property for any purpose within the last two years.

- Any other information relevant for the proper determination of value.

Hotel/Motel:

- Opinion of value as of January 1, 2025, and the information used to form your opinion.

- Number of units, average annual room rate (ADR). RevPar, and occupancy rate for three calendar years prior to the date in question along with three calendar years of income and expense statements.

- If Change of ownership in 2025, provide purchase or sales agreement & closing statements including all addendums. Franchise Agreement, Management Agreement, Franchise Inspection Report, and Product Improvement Plan.

- Description and actual cost of any new construction completed or in progress, during the 2024 calendar year.

- Copy of any appraisal performed on the property for any purpose within the last two years.

- Any other information relevant for the proper determination of value.

REVIEW DUE TO VALUE DECLINE

State law allows the Assessor to temporarily reduce the assessed value of mobile home in certain cases where the fair market value is lower than the assessed value. If this may be the situation for a mobile home you own, request forms are available to view and/or print by clicking below. They are also available by calling or writing the Assessor's Office.

THE DEADLINE TO FILE THIS FORM FOR THE 2025-2026 ASSESSMENT ROLL ENDS AUGUST 1. To apply for a reduction for the 2025-2026 Assessment Roll please visit the Assessor's website after you receive your notification card in June 2025.

Attachements:

About Prop 8

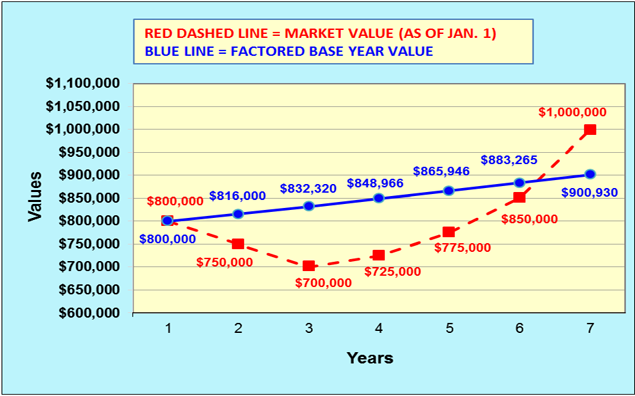

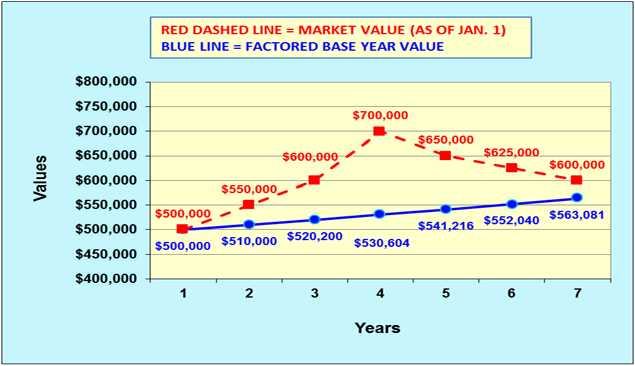

Proposition 8 was passed in November 1978 as an amendment to Proposition 13 and implemented as Revenue & Taxation Code Section 51(a)(2). It annually caps the assessed value of property as of the lien date (January 1) at the lesser of its market value or its factored base year value.

HOW IT WORKS

Proposition 8 allows a temporary reduction when the market value of property has fallen below its factored base year value as of the January 1 lien date. Once a Prop 8 reduction has been enrolled, the property’s assessment must be reviewed annually to ensure that the lesser of the market value or the factored base year value is enrolled.

The property’s base year value continues to be factored at a maximum two percent per year, setting its maximum assessed value. As the market recovers the market value of a property will increase based on market conditions which are not restricted to a two percent growth. The value enrolled will follow the market growth rate until the market value exceeds the factored base year value and the lower factored base year is enrolled.

Factored base year value: the value established as of the date of acquisition and/or completion of new construction. This value is adjusted each year by an inflation factor. The inflation factor is the lesser of 2% or the California Consumer Price Index (CCPI) rate.

For more information about factored base year value, see Understanding Proposition 13.

Related Links:

- Decline In Value Request

- Proposition 8 Request for Review Form (printable)

- Mobilehome Proposition 8 Request for Review Form

- How to File a formal appeal of your assessed value, a how to video

- Why Pay When It's Free!

Attachments